SS1 - Drilling underway at 480m ounce silver equivalent resource

Our silver-gold Investment Sun Silver (ASX: SS1) just started drilling it’s project in Nevada, USA.

SS1 project already massive - biggest pre-production silver asset on the ASX.

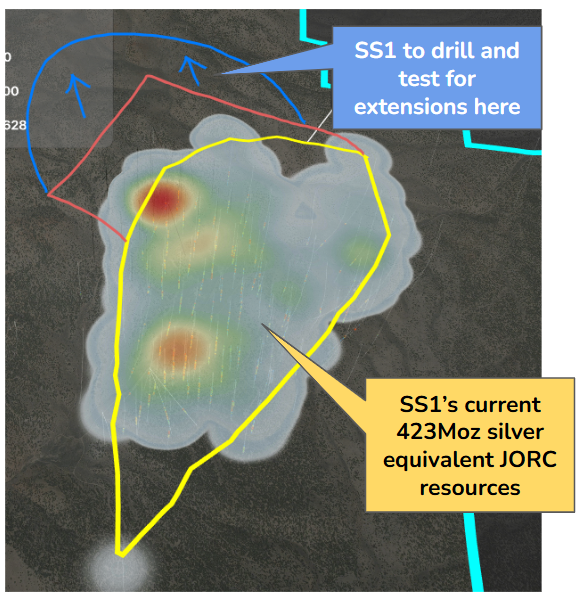

SS1’s resource now sits at 480M ounces silver equivalent.

(2.16M ounces of gold, 296.5M ounces of silver)

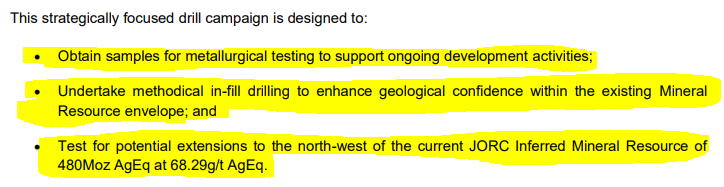

Today, SS1 kicked off a new drill program, which is designed with three overarching objectives:

(Source)

All of the drilling work will form the basis for the following catalysts:

- Metallurgical testwork results - this is basically technical work SS1 needs to do to see if the silver and gold in it’s deposit can be extracted using conventional well understood processing methods. For this one, we want to see high recovery rates using the simplest processing methods.

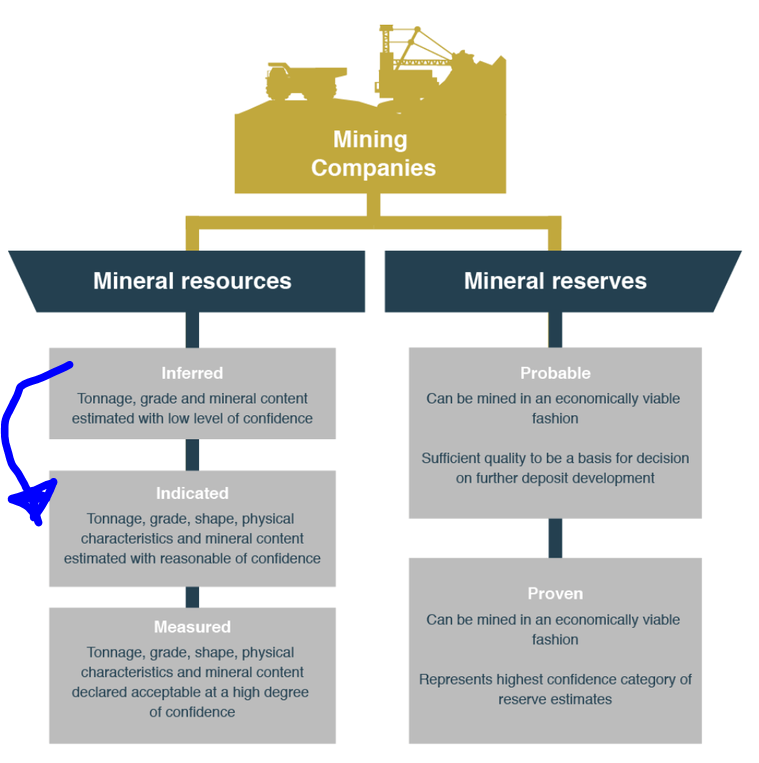

- Resource Upgrade (Classification) - in-fill drilling will be used to upgrade SS1’s resource from inferred into the higher confidence categories (indicated/measured).

- Resource Upgrade (Size) - IF SS1 can hit new extensions to the north-west of its JORC resource, there is potential for the resource to increase further.

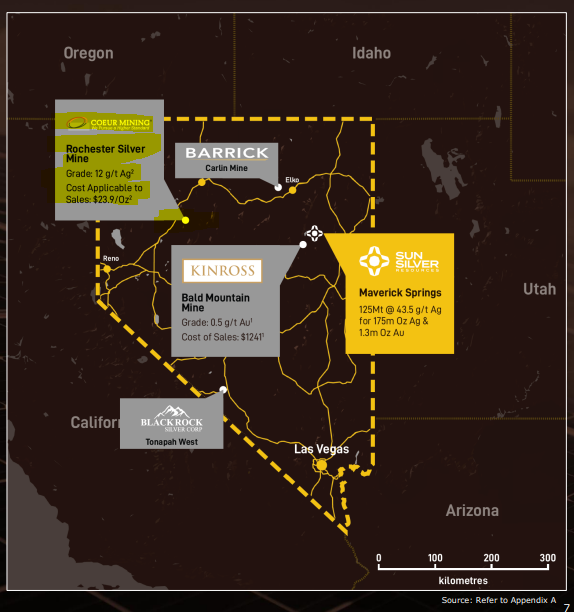

How does SS1’s project rank against other mines in Nevada?

SS1’s project is already very big and we have previously compared it to operating mines in Nevada, USA.

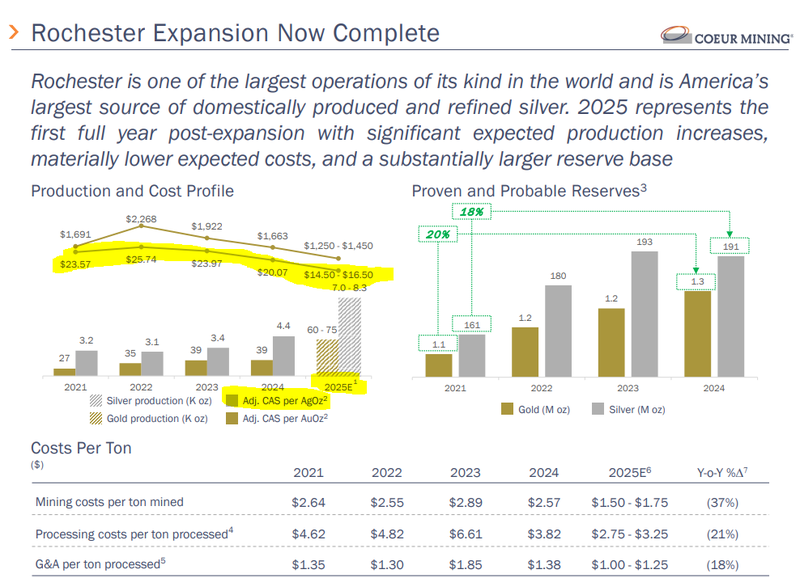

The main comparison we made in our last note was with the Rochester Mine, which is also in the northern half of Nevada.

The Rochester Mine is owned and operated by $4BN capped Coeur Mining which is the world’s largest silver producer.

Rochester is a very large low-grade, easy to mine, easy to process project, and in 2024, the mine produced ~4.4m ounces of silver and ~39k ounces of gold.

Rochester has been producing silver and gold at average grades of ~12g/t.

Compare that to SS1’s resource, which has 0.31g/t gold, 42.2g/t silver (68.29g/t silver equivalent).

Despite the low grades, Coeur has managed to keep its average cost of production at ~US$20 per silver equivalent ounce... well below current spot prices of ~US$33.

AND Coeur is actually forecasting even lower costs in 2025... US$14.50 to US$16.50 for the year.

(Source)

The reason projects in this part of Nevada can be mined at such low costs comes down to a few reasons:

- Because of their geology (“Carlin Style”) deposit - deposits in this part of Nevada are flat lying meaning when a company starts mining the juiciest parts of the orebody, it is big and very consistent over a large area. Size/consistency means predictable costs…

- Because they also produce gold as a co-product - Coeur’s Rochester produced ~39k ounces of gold in 2024. It might not sound like much but it adds to the project’s economics. SS1’s resource similarly has a big gold resource too (~2.16M ounces). At current gold prices that has a big impact on the economics of projects like SS1’s.

- Because they are easy to process - Extraction techniques that are commonly used in the region mean that low-grade gold and silver can be easily extracted. SS1 still has some metwork to do on this front, but that is one of the goals we want to see the company kick in 2025.

The key takeaway is that mineral deposits within the Carlin Trend can be mined at extremely low cost and the Rochester Mine illustrates this.

Our “Big Bet” for SS1 centres around seeing SS1 take its project through the mining company lifecycle and build towards project development.

Our new SS1 Investment Memo

Last month we published our new SS1 Investment Memo which details:

- What SS1 does

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan

To see in detail what we are hoping SS1 can achieve next, check out the memo in full here.